Stanley Black & Decker (NYSE: SWK) stock is down a brutal 63% from its all-time high (reached in the spring of 2021). The sharp drawdown has been the worst sell-off for the blue-chip dividend stock since the 1970s. And Stanley Black & Decker is a far more reputable and established company today. In fact, it’s a Dividend King, which is an S&P 500 component that has paid and raised its dividend for at least 50 consecutive years.

It’s rare for a Dividend King to see a drawdown this far and this fast. And while there are good reasons for the sell-off, there’s also an argument that Stanley Black & Decker stock is wildly undervalued and could be a powerful passive income source for 2023 and beyond.

Image source: Getty Images.

Nuances of the industrial economy

Industrials have been one of the best-performing sectors so far in 2022. The S&P Industrial Select Sector Index is down less than 5% year to date, which is far better than the S&P 500’s 15.5% decline. Long-term investors may be scratching their heads at the industrial sector’s relative outperformance, given that it usually ebbs and flows along with the broader economy and the S&P 500. But 2022 has been no ordinary economy.

What has made this year unique is the disconnect between the health of businesses and the health of the consumer. Demand for new equipment and aftermarket services in agriculture, mining, oil and gas, power generation, and many industries in or related to the industrial economy is strong because commodity prices like oil, natural gas, soy, corn, wheat, and raw materials are doing well. These favorable trends are leading to record profits and near-record high stock prices for companies like Deere & Company and Caterpillar that sell high-ticket equipment and machinery mainly to other businesses.

There’s also the added tailwind of higher U.S. infrastructure spending, which pairs with the trend toward deglobalization as countries look to bring manufacturing back home and improve security. Higher commodity prices combined with these trends are great news for industrial companies that sell products and services to other businesses. But these trends don’t really benefit industrial companies that depend on the health of the consumer.

Enter Stanley Black & Decker, which is vulnerable to consumer spending. Not only has the company been combating a weakening consumer, but it is also dealing with supply chain challenges, rising raw materials costs, and labor challenges. The company is in the process of a reorganization to cut costs and navigate prolonged headwinds. In the meantime, earnings are only slightly higher than they were five years ago. And Stanley Black & Decker currently has negative free cash flow, which means it can’t support its dividend with cash.

Declining financial health

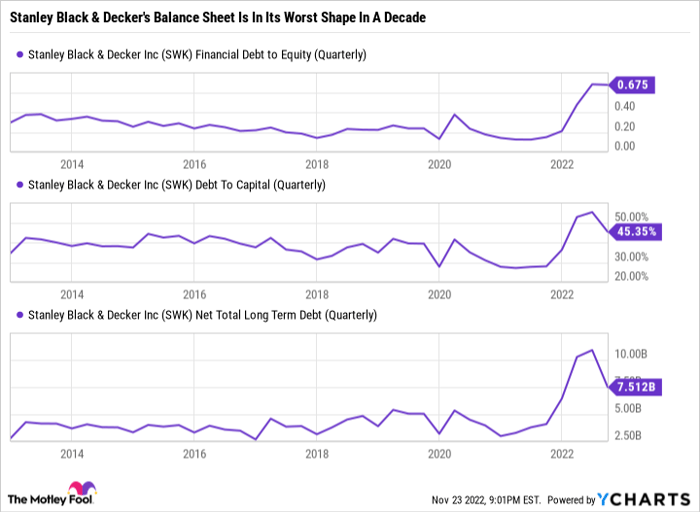

In addition to its poor performance, the health of the company’s balance sheet has declined. Financial debt-to-equity and debt-to-capital are at or near 10-year highs, while total net long-term debt is down off the 10-year high but is still much higher than in past years and more than double levels seen less than two years ago.

SWK Financial Debt to Equity (Quarterly) data by YCharts.

The reorganization should help limit the company’s dependence on debt. But investors are taking a “prove it” approach to the stock, which explains why the sell-off has gone as far as it has.

The good news is that Stanley Black & Decker’s balance sheet was in very good shape at the start of 2021. So as challenges intensified last year and throughout 2022, the company had a hefty margin of error to take on more debt. This margin of error is a common quality of Dividend Kings. To pay and raise a dividend for over 50 years in a row (Stanley Black & Decker has paid but not raised its dividend for 146 consecutive years), a company has to keep a good balance sheet so it can outlast downturns.

Stanley Black & Decker couldn’t have predicted the extent of the challenges it has faced. But it did what it could control, which was to position its balance sheet so that it could take on debt when needed.

A worthy turnaround play

As bad as Stanley Black & Decker’s performance has been, the stock has sold off too far — especially considering the company’s track record for dividend raises and its industry-leading position.

Stanley Black & Decker stock now has a dividend yield of 3.9%, which is the highest level since the great recession of 2008. Stanley Black & Decker has been through past cycles before. The stock looks like a potential turnaround play. And the high dividend yield provides a compelling incentive to hold the stock while waiting for the business to rebound.

10 stocks we like better than Stanley Black & Decker

When our award-winning analyst team has a stock tip, it can pay to listen. After all, the newsletter they have run for over a decade, Motley Fool Stock Advisor, has tripled the market.*

They just revealed what they believe are the ten best stocks for investors to buy right now… and Stanley Black & Decker wasn’t one of them! That’s right — they think these 10 stocks are even better buys.

See the 10 stocks

*Stock Advisor returns as of November 7, 2022

Daniel Foelber has no position in any of the stocks mentioned. The Motley Fool recommends Deere & Company. The Motley Fool has a disclosure policy.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.