India has experienced a structural change in the financial environment of its employees on a salaried basis. The Government of India formally introduced the brand-new Employees Provident Fund (EPF) Scheme, 2026 which replaces the decades old EPF Scheme of 1952, on June 29, 2026. Though this new framework holds the promise of a fully digitized ecosystem, less complex compliance regulations and streamlined interactions of almost eight crore active subscribers under the Employees’ Provident Fund Organisation (EPFO), the fact of inoperative EPF accounts and unclaimed retirement savings raises critical questions about retirement fund management and governance.

As India transitions to the new regulatory framework, the persistence of dormant EPF accounts and unclaimed retirement savings highlights the need for stronger record management, timely account transfers, and improved awareness among employees. Millions of inoperative EPF accounts continue to hold substantial retirement savings that remain unclaimed or unconsolidated, highlighting the importance of timely account transfers and record updates.

What the RTI Investigation Revealed

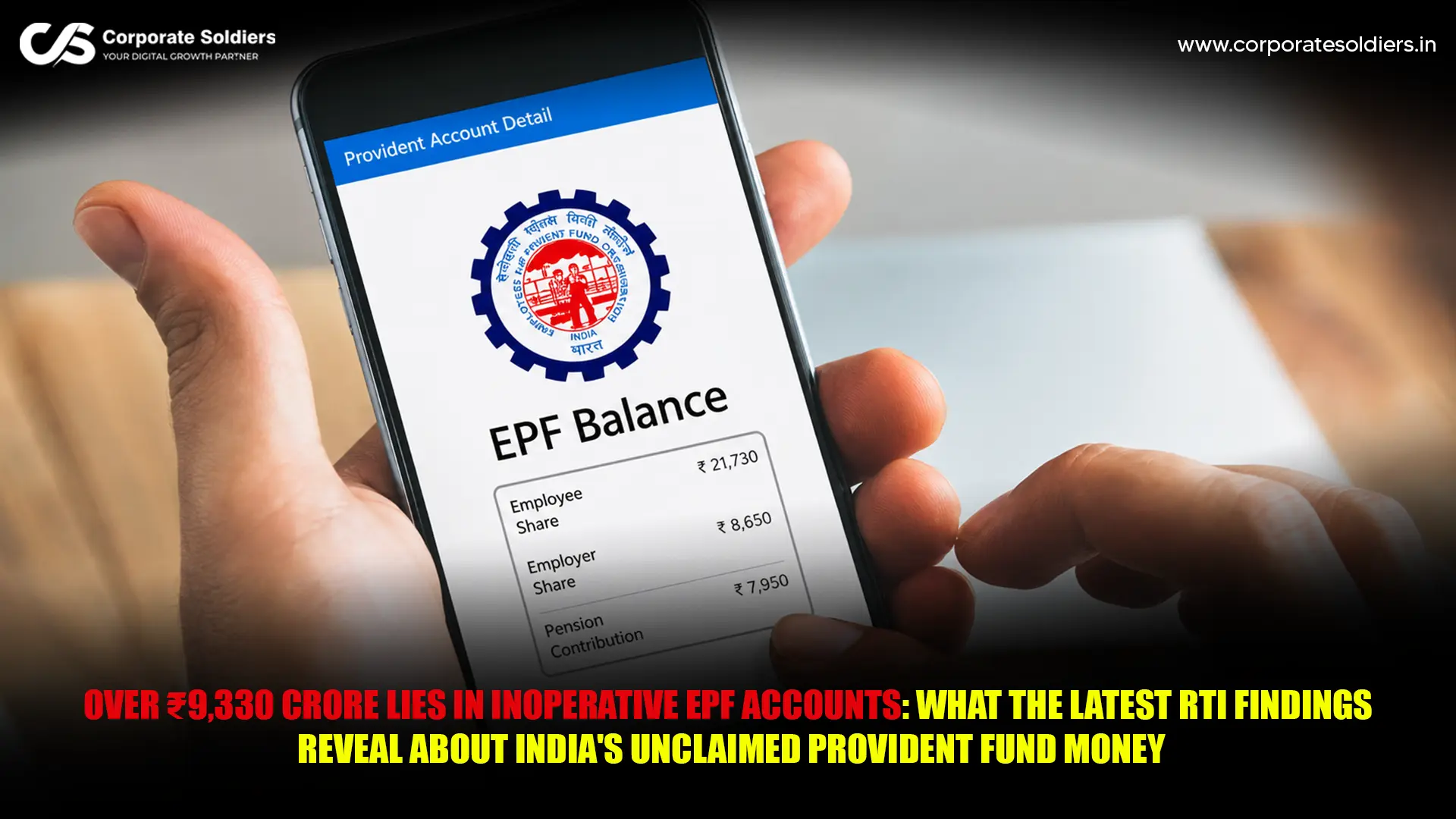

An RTI application has brought fresh insights into the scale of unclaimed EPF balances in India. The data shared by EPFO highlights the continued presence of legacy inoperative accounts despite ongoing digitisation efforts.

Although the amount remains significant, the latest figures show a modest improvement compared with the previous financial year. Comparative analysis of the figures shows that the total number of inoperative accounts decreased about 92,000 accounts within a period of one year – the figure decreased to 30.91 lakh accounts on March 31, 2026 as compared to 31.83 lakh accounts on March 31, 2025. At the same time, the aggregate quantum of unclaimed funds recorded a reduction of ₹851 crore as compared to 10,181 crore recorded at the end of the previous fiscal year.

This idle capital is almost equal to the total amount the central government has spent on the regional airport connectivity scheme, UDAN, since 2016 (about ₹10,169 crore) to put it into perspective in terms of the macroeconomic scale, ₹9,330 crore. Moreover, it equals the seasonal allocations in the Union budget to the key health infrastructure projects such as the Ayushman Bharat-Pradhan Mantri Jan Arogya Yojana (PM-JAY).

For perspective, the estimated cost of establishing an IIT campus was around ₹1,750 crore in 2014. Accounting for inflation, a modern campus would cost approximately ₹2,934 crore today. Based on these estimates, the ₹9,330 crore lying in inoperative EPF accounts is broadly equivalent to the cost of establishing three modern IIT campuses.

With held and Unmaintained Parameters

RTI inquiry tried to reveal the historical patterns of account and the long-run patterns but the limits of data maintenance were encountered:

- Fiduciary Exemptions on Aadhaar Information: The application explicitly required an account by account breakdown of inoperative accounts already attached with Aadhaar, and their auto-settlement clearance rates. The EPFO refused to disclose these fields as it violated Section 8(1)(e) of RTI Act, 2005, which protects information that is stored in a fiduciary position by a government agency.

- Lack of Long-Term Historic Trends: When inquired about a one-year on another historical trend over the past six years of financial performance, the EPFO responded that it only has easily available data on 2025 and 2026. The authority observed that its special Inoperative Accounts Cell (IAC) was not established until the 20252026 era, and previous consolidated records were not in this institutional form.

- High-Value Thresholds: The EPFO also suggested that it does not have centralized datasets that are in a format to filter out the number of inoperative accounts with individual balances of ₹5 lakh and above.

What Is a Dormant EPF Account?

To understand why billions of rupees remain unclaimed, it is important to understand how EPFO classifies an account as inoperative. Under the EPF Scheme, 2026, an account’s status depends on an employee’s contribution history and employment status.

| Account Category | Regulatory Definition & Operational Status |

| Active Account | Receives regular monthly statutory contributions from both the employer and the employee. Fully linked with an active Universal Account Number (UAN). |

| Inactive / Inoperative Account | An account where contributions have completely ceased, typically following an employee’s retirement, permanent migration abroad, or cessation of employment without a formal transfer request. |

| Unclaimed Corpus | Funds remaining within an inoperative account that have not been pulled out or merged by the member or their legal nominees over extended multi-year periods. |

An account is officially put into an inoperative state with the following specific parameters:

- In the case of a member who retires permanently out of service when he/she reaches the age of 55 years.

- In the event a member permanently migrates to a foreign country.

- Should the subscriber die, in the unfortunate event.

- In the event when a member quits employment and does not make a formal application to transfer online EPF or make final withdrawal within the specified time, abandoning the balance in the legacy.

The Interest Accumulation Paradigm

One of the most confusing aspects to personal finance consumers is whether or not idle accounts are still receiving compound interest. In 2016, under historical amendments, the Ministry of Labour and Employment made it clear that interest accrual would not be suspended with regard to inoperative accounts of employees who do not yet attain retirement age.

But beyond the point of formal retirement age (55 years) when a subscriber reaches that age, incremental interest does not accrue on the account after a long period of complete non-contribution. Since then the frozen balance has been technically an unclaimed fund. When the balance is left in any of the designated institutional accounts, which was not entirely claimed in over 7 years under the Senior Citizens Welfare Fund, they may be subject to redirection to the public welfare corpuses, but they are legally claimable by the owner who has verified ownership by submitting genuine evidence.

Why So Much EPF Money Remains Unclaimed

The 3.09 million accounts totaling more than ₹9,330 crore are not caused by a single systemic failure, but the actions and historic administrative loopholes.

Frequent Job Changes

The modern business environment promotes inter-company fluidity. When the professionals move quickly they often end up neglecting the administrative role of balancing up their legacy balances. Traditionally, all individual employment events have led to the creation of an individual, siloed Member ID, splitting the personal site of retirement savings, prior to the full implementation of the centralized database.

Failure to Update KYC

One of the essential conditions prior to any financial settlement in India is complete Know Your Customer (KYC). There are thousands of old accounts that contain outdated records, an incorrect middle name or primary identity records that have not been verified. When such a person tries to get these funds several years later, automated verification mechanisms raise these anomalies, and people simply give up the process as it leads to perceived friction in the procedure.

Missing UAN Linkage

Universal Account Number (UAN) was designed to be a life-long general identifier of an EPF journey of a citizen. But millions of accounts which were already open before the full roll-out of the UAN system are not yet linked. The former employees who have worked in the early 2000s, tend to have a physical slip record of having an obsolete Member ID but without a digitally mapped UAN to kick start an online consolidation.

Lack of Awareness

Most of the entry-level corporate workers consider EPF as a monthly line-entry deduction to their paychecks that they do not think about at all, and its compound interest possibilities. In a few cases, employees totally lose track of balances that they build up in short-term jobs at the beginning of their careers.

Nominee Issues

The lack of an updated digital nomination will be a major obstacle in case of the untimely death of a subscriber. In the event of the failure of the employee to submit an e-Nomination through the official portal, his or her legal heirs or dependents would have to go through complicated legal procedures e.g., issue succession certificates or letters of administration cleared by the court, in order to get access to the legacy funds.

Documentation Errors

Mismatch in main data items is still a significant challenge. Basic clerical errors in entry-transposing some numbers in a date of birth, misspelling a surname or moving between pre- and post-marriage name- preclude automated cross-matching of the EPFO database and existing identity cards.

EPFO’s Position on Inoperative EPF Accounts

The institutional position of EPFO points out that the unclaimed money is absolutely safe and it is still the property of the worker who contributed it or his/her rightful heirs. EPFO states that eligible members or their legal heirs can claim EPF balances by following the prescribed claim and verification process under the applicable rules.

To address the issue of over ₹9,330 crore lying in inoperative accounts, EPFO has put in place several institutional measures:

Inoperative Account Cell (IAC): This specialized division was formally operationalized as part of the 202527 cycle, whose responsibility is to determine long-standing dormant balances, to fix data linkages, as well as to establish mechanisms to reconcile the historical corporate records with individual identities.

Implementation of the EPF Scheme, 2026: The revised framework seeks to strengthen digital account management, simplify provident fund administration, and make it easier for members to manage their EPF records and account transfers.

How Employees Can Check Their EPF Status

Salaried professionals should conduct regular audits of their historical provident fund records. The EPFO has built several digital interfaces designed to help citizens trace their past accounts.

[EPFO Portal Audit] ──> [Verify UAN Activation] ──> [Check Passbook for Idle Balances] ──> [Trigger Online Transfer]

- The Unified Member Portal

To check the details of their accounts, the subscribers should address the official EPFO Member Portal:

- Enter a platform with an active 12-digit UAN and password.

- Go to the ‘View’ tab and choose Service History.

- Go through the detailed history of all the Member IDs associated with your career. Any history ID account, which displays an un-transferred balance, needs to be integrated at once.

- The EPFO Member Passbook Facility

Users can also check precise balance with the help of the special passbook microsite:

- Log in with usernames and captcha authentication.

- The system has unique dropdowns of each registered Member ID.

- Check each ledger to determine whether or not past employer balances have been brought to a zero balance through an official transfer, or whether they include idle, un-transferred balances.

- The UMANG Application

In the case of mobile-based checks, UMANG has an app provided by the Government of India:

- Register and complete your profile on the UMANG application.

- Choose institutional service module- EPFO.

- To get a breakdown of your current and past employee balances on your mobile screen, click on View Passbook and get an OTP-authenticated breakdown.

- Cross-Verification of Critical Links

Make sure that your UAN profile meets three main digital parameters:

- Identity Check: Make sure that your online profile and the identity documents are a perfect match.

- Mobile Seeding: You will have to use the same mobile number that is associated with your UAN to make sure that OTP is delivered without any gaps.

- Bank Account Authorization: Seed your active bank account number, and IFSC within the portal and authorise it digitally by your current employer using an electronic signature.

How to Claim Funds from an Inoperative EPF Account

To reclaim money in an inoperative, or dormant account, there are certain steps that one must take based on the accessibility to a UAN.

Scenario A: If a UAN Exists and Past Accounts are Discoverable

In case you have an active UAN, but you find that an old Member ID has an un-transferred balance, you may start a digital consolidation:

- Log in to the EPFO Unified Member Portal.

- Go to the menu called Online Services, and choose One Member One EPF Account (Transfer Request).

- Confirm your personal information, as well as the details of the current account.

- Click on Get Details to enter your past records of employment in the system.

- Choose your former employer or the present employer to endorse and claim the transfer form, based on your current relationship with the HR.

- Verify the transaction by an OTP that is sent to your registered mobile phone. The system is then sent to the employer to be digitally signed and the balance in the legacy is transferred into your active account.

Scenario B: If the Account is Very Old and Lacks a UAN

In the case of legacy accounts that were created before 2014, and no UAN is assigned:

- Find Historical Credentials: Find the alpha-numeric establishment code and individual extension number, by retrieving old corporate payslips or annual physical PF statements to determine the specific alpha-numeric establishment code and individual extension number.

- Employer Coordination: The official EPFO document repository will provide Form 13 (to transfer) or Form 19 (to withdraw final settlement) that should be downloaded. Enter the particular parameters manually.

- Attestation Protocol: In case the legacy enterprise is either closed down or cannot be accessed at all, then the physical application is supposed to be attested by a qualified official. Authorities allowed are a Gazetted Officer, a Bank Manager of the branch where you have an active account or a local Magistrate.

- Physical Submission: Submit the authenticated physical dossier at the regional EPFO field office in which the past employer’s historic head office has jurisdiction over your past workplace.

Why Inoperative EPF Accounts Matter

Nearly ₹9,330 crore held in inoperative EPF accounts has significant implications for individual retirement security and overall provident fund administration.

Individual Retirement Security

The balances of the provident funds are based on the concept of long-term compounding. When a person does not invest a balance of ₹50,000 in the old account, which later ceases to earn interest, he/she loses a lot in future. That one untransferred amount would have grown manifold in the course of a 25-year career, had it been put into an active, interest-bearing account.

Domestic Household Savings Rate

The cornerstone of long-term institutional capital in India is made up of retirement corpus. When billions of rupees remain locked in inoperative accounts because of identity mismatches or administrative delays, those funds remain disconnected from members’ active retirement savings.

Governance and Public Trust

An increase in unclaimed stock of the commonwealth capital may be a source of administrative tension to charity organizations. Having the savings of hard-earned retirees returned to their legitimate owners effectively is a way of building systemic confidence in statutory savings programs.

Expert Perspective on EPF Governance

The transition to the EPF Scheme, 2026 reflects the government’s broader effort to modernise provident fund administration through greater digitisation and simplified processes. However, the RTI findings indicate that resolving legacy issues such as incomplete records, outdated KYC details, unlinked Member IDs, and inoperative accounts will continue to require sustained administrative efforts by EPFO as well as timely action from employers and employees.

What Employees Should Do Immediately

To secure your retirement income, the following seven steps are the basic steps to be undertaken by salaried professionals:

- Gather Your Documents: Find all of your historic employment letters and payslips of all the jobs you have worked in.

- Check Universal Account Numbers: Make sure that you do not have two or more UANs. In case you possess two or more UANs in various occupations, log in to combine them and fuse them instantly into one.

- Complete Full e-Nominations: Do not leave your online profile without a new nomination. Fill in the e-Nomination form online using definite percentage shares of your beneficiaries to ensure the future of your family has access to it.

- Check Your KYC Data: Verify your UAN dashboard by taking note of the fact that your name, father name, gender and date of birth are exactly the same as that of your primary identity cards down to the letter.

- File Electronic Transfer Applications: In case of any unlinked legacy Member IDs with residual capital, you can request the transfer of these funds online into your active account.

- Keep Recent Contact Details: Have your main mobile number up-to-date on the portal so that you never miss systemic alerts, interest notifications, and OTPs.

- Keep Enterprise Documents offboarding: It is best to keep your hardcopy relieving letters, experience certificates and physical PF information always when you are leaving a job.

What Happens Next

The implementation of the EPF Scheme, 2026 marks an important step in the government’s efforts to modernise provident fund administration through greater digitisation and simplified compliance. EPFO has also been expanding digital initiatives to improve record management, strengthen member services, and make account transfers more efficient.

At the same time, the recent RTI findings highlight that addressing legacy inoperative accounts will require continued improvements in data management, timely account consolidation, and greater awareness among employers and employees. As EPFO continues to expand its digital initiatives, improving record management and facilitating account consolidation are expected to support the resolution of legacy inoperative accounts over time.

Final Thoughts

The findings from the recent RTI disclosure show that while the EPFO is modernizing its digital platform, bridging legacy gaps remains a major priority, with over ₹9,330 crore still sitting in 30.91 lakh inoperative accounts. This stranded capital is a clear reminder that long-term retirement security depends as much on diligent administrative follow-through as it does on monthly savings.

As the new EPF Scheme, 2026 takes root across India’s corporate sector, salaried professionals, corporate leadership teams, and HR managers must work together to clear these legacy backlogs. By proactively auditing your digital profiles, resolving documentation errors, and consolidating old accounts, you ensure your hard-earned savings remain active, secure, and fully optimized for your retirement years.